3 Financial Statement Analysis

FINANCIAL STATEMENT ANALYSIS: “HOW ARE WE DOING?”

Financial statement analysis informs a wide variety of strategic management questions, including:

- What is this organization’s overall financial position? Is it liquid? Profitable? Solvent?

- How does this organization’s financial position compare to its peer organizations?

- How much debt or other long-term liabilities can this organization afford?

- How can this organization adjust its operations and policies to strengthen its financial position?

On March 22, 2014, the side of a hill near the town of Oso, Washington, gave out after three days of relentless rainfall. A massive landslide followed, with mud and debris covering more than a square mile. Forty-three people were killed when the slide engulfed their homes.

In the days that followed, more than 600 personnel participated in search and recovery operations. They rescued eight people from the mud and evacuated more than 100 others to safety. Most of the rescue personnel came from the four rural Snohomish County fire districts surrounding Oso.

Minutes after hearing of the slide, staff at the Washington State Office of Financial Management (OFM) – the governor’s budget office – made two critical phone calls. Earlier that week, they had reviewed some data on the financial health of local special districts across the state. They observed that rural fire districts in the counties north of greater Seattle showed signs of acute fiscal stress. Those districts had seen huge growth in property tax collections during the real estate boom of the 2000s. But since the real estate crisis of 2007-2009, those revenues had fallen precipitously. Many of these districts had laid off staff, cut back on specialized training, and back-filled shifts with volunteer firefighters.

So, moments after hearing of the slide, OFM staff called the fire chiefs at two of the most financially stressed Snohomish County fire districts. Their message to those chiefs was simple: send your people. OFM agreed to reimburse the districts from state or federal emergency management funds if needed. In turn, personnel from two of those districts were among the first on the scene and were responsible for three of the eight life-saving rescues.

A few weeks later, the chiefs of both those districts acknowledged that had OFM not called, they would not have sent their personnel. Both districts were so financially stressed that they could not have afforded the overtime wages and other expenses they’d have incurred to participate in the rescue operations.

Financial condition matters. It shapes how a public organization thinks about its mission and capacity. In the case of the Oso mudslide, it was the focal point for some life-saving decisions. That is why all aspiring public servants need to know how to evaluate financial statements and measure, manage, and improve their organization’s financial position.

LEARNING OBJECTIVES

After reading this chapter, you should be able to:

- Compute and interpret ratios that describe liquidity, profitability, and solvency. Contrast how those ratios mean slightly different things across the government, non-profit, and for-profit sectors.

- Understand the typical strategies organizations employ to improve their liquidity, profitability, and solvency.

- Contrast short-term solvency with long-term solvency, particularly for governments.

What is Financial Position?

Financial position is a public organization’s ability to accomplish its mission now and in the future. When stakeholders ask, “How are we doing financially?” the answer should reflect that organization’s financial position.

An organization’s financial position has three main components:

- Liquidity. Does the organization have liquid resources to cover its near-term liabilities?

- Profitability. Do the organization’s revenues cover its operating expenses?

- Solvency. Can the organization generate enough resources to cover its near-term and long-term liabilities?

In the previous chapter, you learned how to extract information about an organization’s financial position from its balance sheet. For example, are most assets liquid (e.g., cash and marketable securities), or does the organization have assets that are more difficult to convert to cash (e.g., receivables, inventory, or prepaid expenses)?

The balance sheet also tells us a lot about solvency, namely if the organization has a lot of long-term liabilities (e.g., long-term debt or pension liabilities). Long-term liabilities mean the organization will have to divert some of its resources to meet those obligations, which can mean fewer resources to invest in its mission. To be clear, there are times when an organization can and should take on long-term liabilities in pursuit of its mission. Sometimes it makes sense to borrow and invest in a new facility that allows the organization to serve its clients effectively. Pensions and retiree health care benefits are an important employee recruitment and retention tool, even though offering current and future employees these benefits could result in a long-term obligation.

To learn about profitability, we typically look to the income statement. Recall that if an organization’s revenues exceed its expenses, its net assets will grow. The income statement clarifies the organization’s key sources of revenues, which revenues are growing, and whether those revenues cover program and administrative expenses. The income statement also shows depreciation, bad debt expenses, and other expenses that reduce net assets but do not impact cash. These are all solvency considerations.

While financial ratios can provide useful metrics, always start with a quick review of the financial statements. Ideally, the financial statements you are working with should report on the organization’s operating and financial position for at least two financial periods – though that is not always the case. Keep in mind that funding agencies and financial analysts need access to at least four, if not five years, of financial data. A review of the trends should inform your interpretation of the ratios.

A review of the Statement of Financial Position (or Statement of Net Position) can be guided by the following questions:

- Assets: How have the assets changed? What proportion of assets are current? How much is reported under cash and cash equivalents? How much is reported under property plant and equipment, net of depreciation? Were there any new investments in property, plant, and equipment (review note on fixed assets)? How much is reported in investments? What proportion of investments are restricted? Have investments changed significantly, and was this the result of market gains and investment income, a capital campaign, or transfers from cash? How much more or less is the organization reporting in receivables, prepaid expenses, or inventory? Have changes in current assets had a negative or positive impact on cash flows?

- Liabilities: How have the liabilities changed? What proportion of liabilities is the result of operations? What proportion of liabilities is current? What proportion of liabilities is the result of financing activities? Of that, how much is in the form of a short-term loan or a line of credit? Is the organization subject to loan covenants or restrictions, and are these disclosed in the notes to the financial statements? Are there any contingent liabilities because of recent lawsuits, and what is the probable liability?

- Net Assets: What proportion is reported as net assets without donor restrictions? What proportion is reported as net assets with donor restrictions? Of net assets with donor restrictions, what proportion is reported as permanently restricted (review notes on Endowment funds)?

Similar questions can guide your review of the Statement of Activities:

- Revenues: What are the major sources of revenues? Were there significant changes in operating revenues? Of total revenues, what percent is “with donor restrictions”? What proportion is contributed versus earned (e.g., fee for services, government contracts)? How much does the organization report as foundation grants? Corporate gifts? Is the organization susceptible to changes in governmental agency or foundation funding priorities?

- Expenses: How much did the organization spend on programs? How much did the organization spend on administration? Fundraising? Were there significant changes in the level of spending? What proportion of our expenses are personnel costs? Have personnel costs changed? How much did the organization report in depreciation and amortization? Are there other fixed costs that limit budget flexibility?

Financial Statement Ratios

The purpose of accounting is to help organizations make better financial decisions. Financial statement analysis is the process of analyzing an organization’s financial statements to produce new information to inform those decisions. Public organizations make dozens of crucial decisions every day: Should we expand a program? Should we lease or buy a new building? Should we move cash into longer-term investments? Should we accept terms in a contract with a government agency? Should we accept a grant with restrictions from a foundation? Should we, as a funding agency, fund a particular organization?

These decisions can be informed by financial statement analysis. An organization should only expand if its existing programs are profitable. It should invest in new property or equipment once it understands how existing fixed asset costs contribute to or detract from its net position. It should move cash into less liquid investments once it knows the organization has sufficient liquid resources to cover its operating expenses.

To answer these questions, we need metrics that demonstrate an organization’s liquidity, profitability, and solvency. We turn to financial ratios (sometimes called financial statement ratios) for those metrics. Financial ratios are calculations derived from information included in the financial statements. Each ratio illustrates one dimension of an organization’s overall financial health. Analysts who evaluate public organizations’ financial statements employ dozens of different financial ratios. However, the way they use ratios will be unique to their needs. For example, the criteria used by financial institutions (or credit rating agencies) will differ from those used by funding agencies. In other words, context and goals matter.

Therefore, a word of caution is necessary when it comes to financial ratios. For many, financial statement ratios objectively assess the organization’s financial position and overall performance. However, when applied incorrectly, they can lead to improper allocation of resources within an organization. For example, focusing on profit maximization, particularly on programs that do not align with the organization’s core values or mission, could lead to mission creep.

Relatedly, criteria used to assess the organization’s financial health should not be the sole criteria used to determine a non-profit’s eligibility for a grant or contract. As you’ll see below, financial ratios are objective measures of financial position and performance that do not incorporate an organization’s proven track record in service delivery. Financial ratios emphasize the organization’s financial strengths and do not address the organization’s effectiveness. Financial ratios do not relay the organization’s unique challenges, or the efforts management and staff have undertaken to address those challenges. In fact, the widespread use of ratios has resulted in widespread inequity in philanthropic giving. Research shows that Black-led organizations receive less funding and are more likely to receive funding with restrictions when compared to peer white-led organizations. As a result, these organizations report low cash reserves, frequently report operating deficits, and often report fewer net assets without donor restrictions. Continued use of financial ratios as criteria for funding organizations perpetuates the cycle – well-funded organizations continue to receive funding without restrictions. In contrast, smaller organizations in poor financial health receive less or restricted funding.

We apply a similar word of caution when using ratios to assess the financial health of governments. A careful review of budget documents or related socio-economic or legal environments would give users a better understanding of why the government reported a deficit or high debt burden. And as we discuss later in this chapter, governments need not be profitable to continue operations.

So, while we endorse the use of financial ratios, we recognize there are limits to their usability and encourage users to contextualize their analysis to the organization, industry, and region of operations.

ADDRESSING RACIAL BIAS IN PHILANTHROPY AND GRANTMAKING

Philanthropy has proven itself as a powerful mechanism for working toward a more equitable society by challenging oppression and seeking to ensure social, economic, and political change (Powell, 2015). But biases based on race, gender, and other factors are still a real problem in the sector, often in the form of implicit bias. Implicit bias refers to the attitudes or stereotypes that affect our understanding, actions, and decisions in an unconscious manner. These biases, which encompass favorable and unfavorable assessments, are activated involuntarily and without an individual’s awareness or intentional control.

Implicit bias in philanthropy affects not just which groups get funded but also who sits on the boards of philanthropic organizations, how grantmaking foundations set priorities, how decisions are made, who makes those decisions, and even who gets hired (Powell, 2015). A D5Coalition 2016 report found that 92 percent of foundation CEOs were white, 83 percent of full-time executive staff were white, and 68 percent of program staff were white. Studies have shown that three-quarters of white people have entirely white social networks, a factor that further excludes organizations led by people of color from philanthropic networks (Dorsey et al., 2020). The D5Coalition report also found that only eight percent of grants were directed to organizations that served diverse communities.

A 2020 study (completed by Echoing Green and Bridgspan) found that Black-led organizations were more likely to receive less funding, receive restricted grants, and were required to meet rigorous reporting requirements. Undoubtedly, the lack of unrestricted support reflects a lack of trust in organizations led by people of color (Dorsey et al., 2020). Over time, disparities in revenue and restrictions result in few net resources that do not have donor restrictions. Data shows that Black-led organizations reported a net asset position without donor restrictions that was 76 percent less than white-led organizations. Additionally, data shows organizations led by Black women consistently receive less support than either Black men or white women. Disparities persist even considering factors like issue area, education level, and gender.

Financial metrics (e.g., revenue growth, demonstrated operating performance, and accumulated reserves) are frequently used to determine organizations with the “capacity” to manage grants, discounting the value of the organization’s work. Using financial health criteria to determine who receives funding perpetuates a vicious cycle, further depriving chronically underfunded organizations that have the potential to do good work!

So, what should funders do? Below are some recommendations based on our review of the existing research. Our list is not comprehensive – we have included an extensive list of readings at the end of this section.

-

Focus on organizational strengths. Assess the organization’s proposals based on its ability to do the work, not trends in revenues or whether the non-profit has reserves or an endowment. Allow for a narrative contextualizing the non-profit’s operating environment and financial history. Understand all the financial and non-financial resources the organization mobilizes to achieve its mission and endeavor to value the work being performed. Funders should provide unrestricted capacity-building grants to strengthen organizational leadership and management and eliminate matching grant requirements, as these requirements marginalize organizations that lack the fundraising capacity and unconsciously steer funding to well-resourced organizations with accumulated resources or access to fundraising networks (Nonprofit Finance Fund, 2019).

-

Cover full costs. Recognizing overhead costs is essential for the proper function of any organization. Smaller organizations do not benefit from economies of scale and, as a result, report higher-than-average overhead costs (median ratio of 20 percent). Larger organizations, especially those with a regional presence or brand recognition, have the capacity to raise public support from individual donors. In contrast, smaller organizations do not have a large or wealthy donor base or the capacity to create one. Understand operational context and challenges. For example, non-profits that rely on government contracts are more likely to be chronically underfunded, as governments rarely cover overhead costs. To that end, funders should consider providing capacity-building grants, as these investments position the organization to deliver higher-quality services beyond the life of the grant.

-

Shift focus from reporting to engagement. Evaluate whether reporting requirements are grounded in organizations demonstrating results or distrust of leaders. Funders should streamline grant application processes and eliminate redundancies in reporting. Where possible, shift the funding model away from restricted annual grant awards to unrestricted multi-year grants, demonstrating the funder’s trust and investment in the organization. Engage with grantees in tangible ways other than grant reports and develop relationships that are not contingent on funding. Build grantee capacity by providing additional funding to smaller organizations to meet reporting requirements and create reporting mechanisms that result in program metrics relevant to both the grantor and grantee.

-

Give more – much more! Foundations consistently use the five percent payout rule as a maximum level of giving, even though the tax law established the five percent payout rule as the minimum. Data shows that even though foundation wealth has nearly doubled since the Great Recession, the level of giving did not change significantly over the period. A philosophical shift that puts “spending decisions within the context of mission” rather than “mission in the context of available resources” shifts the focus away from wealth accumulation and perpetuity of foundations to investing in mission-aligned priority areas at levels that would lead to sustained changes. Additionally, foundations should diversify their grantee portfolio. They should invest in smaller organizations led by Black, Indigenous, or people of color that work in communities that face funding disparities.

-

Make diversity, equity, and inclusion a top priority. The world of philanthropy relies on relationships. Whom you know and who knows you matter! Philanthropic organizations committed to social, economic, and political change lack the lived experience of people of color in low-income communities. Funding organizations should prioritize diversifying their organization, from the non-profit board to the program staff. They should expand their grantee sourcing mechanisms and intentionally reach out to smaller grassroots organizations whose programming and values align with foundation priorities. Finally, they need to be accountable to themselves and the community they serve. To that end, they should report on their diversity, equity, and inclusion goals, benchmarks, and progress.

Our knowledge of implicit bias in philanthropy benefited from the work of many, including Cheryl Dorsey, Jeff Bradach and Peter Kim. (2020). Racial Equity and Philanthropy: Disparities in Funding for Leaders of Color Leave Impact on the Table (Echoing Green and The Bridgspan Group), D5Coalition (2016) “State of the Work: Stories from the Movement to Advance Diversity, Equity, and Inclusion,” John A Powell (2015) “Implicit Bias and its Role in Philanthropy and Grantmaking” and Non-profit Finance Fund (2019) “Addressing Racial Biased Financial Analysis.”

The first table lists a set of liquidity ratios. Recall that liquidity is the ease with which an asset can be converted to cash with minimal loss in value. Liquidity ratios assess liquid assets that can cover the organization’s obligations or day-to-day expenses. The numerator in these ratios measures liquid resources – either current assets or a specific type of current asset (e.g., cash and cash equivalents, receivables, etc.). The denominator is a measure of existing obligations – either current liabilities or average daily cash expenses. To estimate average daily expenses, we take total expenses and deduct expenses like depreciation, amortization, and bad debt expense that do not require an outflow of liquid resources. Our estimate of cash expenses is then divided by 365 days to produce a rough measure of average daily cash spending.

For governments, the focus is on the General Fund. Recall that the General Fund accounts for unrestricted resources or resources that are not required to be accounted for in other funds. The unassigned fund balance is the most closely watched number in governmental accounting. It reports on the government’s unrestricted resources.

FINANCIAL STATEMENT RATIOS FOR LIQUIDITY |

||||

RATIO |

WHAT IT TELLS US |

NON-PROFIT |

GOVERNMENT |

FOR-PROFIT/HYBRID |

Current Ratio |

Will near-term assets cover near-term obligations? Rule of Thumb: >2 | Current Assets / Current Liabilities | General Fund Assets / General Fund Liabilities | Current Assets / Current Liabilities |

Quick Ratio |

Will the most liquid assets cover near-term obligations? Rule of Thumb: >1 | (Cash + Investments + Receivables) / Current Liabilities | (Cash + Investments + Receivables) / Current Liabilities | |

Cash Ratio |

Will cash and investments cover near-term obligations? Rule of Thumb: >1 | (Cash + Investment) / Current Liabilities | (General Fund Cash + General Fund Investments ) / General Fund Liabilities | (Cash + Investments) / Current Liabilities |

Days of Cash on Hand |

How many days of cash do we have? Rule of Thumb: >90 days | (Cash + Investments) / ((Total Expenses – Depreciation – Bad Debt Expense) / 365 days) | (Cash + Investments) / ((Total Expenses – Depreciation – Bad Debt Expanse) / 365 days) | |

Days of Liquid Net Assets |

How many days of liquid net resources do we have? Rule of Thumb: >180 days | (Net Assets Without Restrictions – Fixed Assets, Net of Depreciation) / ((Total Expenses – Depreciation – Bad Debt Expense) / 365 days) | (Net Assets Without Restrictions – Fixed Assets, Net of Depreciation) / ((Total Expenses – Depreciation – Bad Debt Expense) / 365 days) | |

Receivables Turnover |

How long does it take us to collect receivables? Rule of Thumb: <60 days | Receivables / (Revenues / 365 days) | Receivables / (Revenues / 365 days) | |

Short-Run Financial Position |

How much in unrestricted resources do we have as a percent of our revenues? Rule of Thumb: >5% | Unassigned General Fund Balance / General Fund Revenues | ||

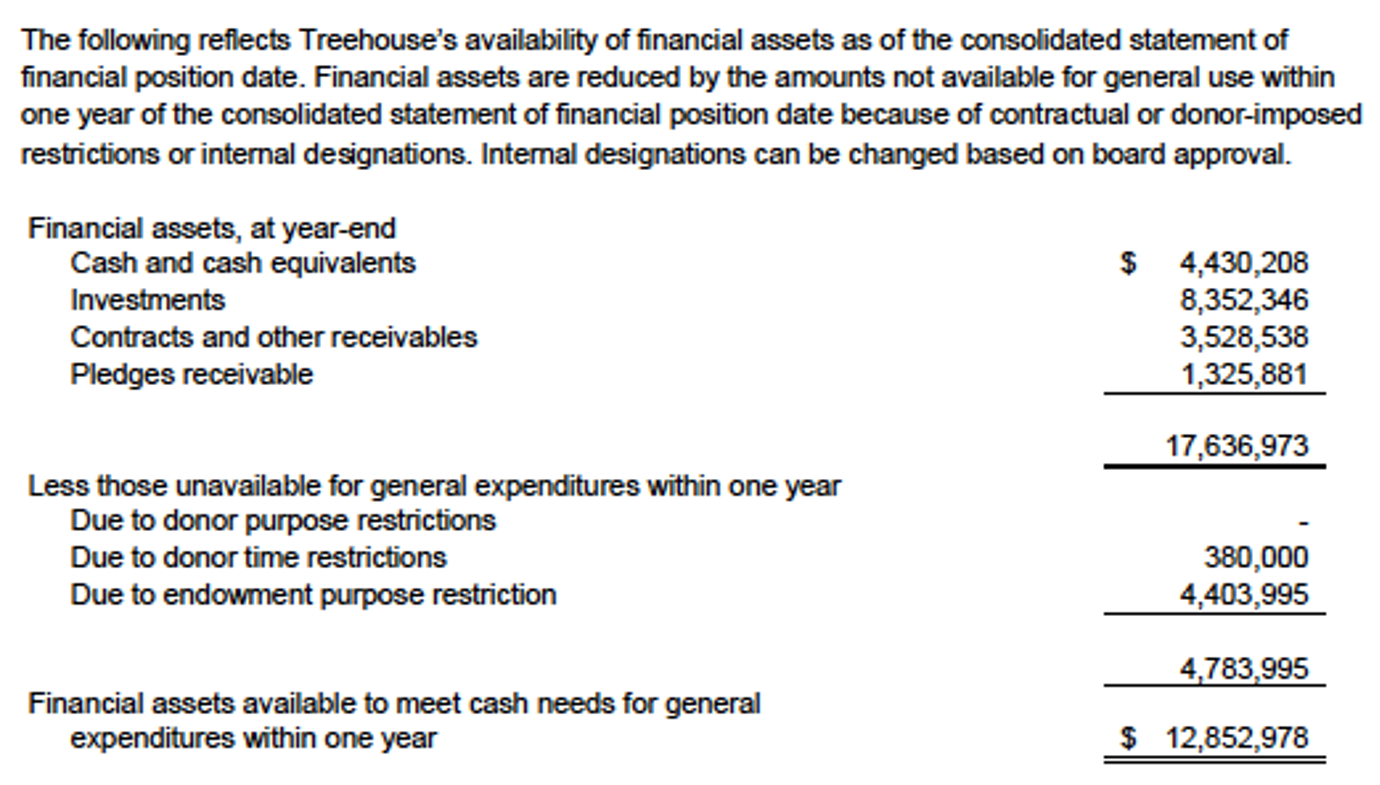

LIQUIDITY AND AVAILABILITY OF FINANCIAL ASSETS DISCLOSURE

FASB Accounting Standards Update No. 2016-14 requires non-profits to disclose qualitative (narrative) and quantitative (numeric) information about their liquidity and availability. According to the standard, the most basic measure of liquidity is the “availability of resources to meet cash needs for expenses within one year of the date of the statement of financial position.” The availability of a financial asset may be affected by (1) its nature, (2) external limits imposed by donors, grantors, laws, and contracts with others, and (3) internal limits imposed by the governing board. Qualitative information communicates how the non-profit entity manages its liquid resources to meet cash needs for expenses. In contrast, quantitative information communicates the availability of the non-profit’s financial assets to meet cash needs for expenses – all within a year of the balance sheet date.

Although common sense tells us that having more assets available for use without limitations allows for greater flexibility to meet unforeseen financial circumstances, it does not immediately follow that a not-for-profit organization that shows a relatively small portion of its assets as “available for general expenditure” is experiencing financial difficulty.

Non-profits routinely use assets received with donor restrictions in ongoing programmatic and operational activities. In those cases, assets that appear to have limitations are, in fact, being put to immediate use paying for day-to-day operations. The narrative disclosure should give financial statement users insight into the full range of assets available for use.

Non-profits may also describe established operating reserve policies, how they manage cash based on major receivables cycles, and the availability and use of lines of credit. When contemplating liquidity disclosures, NFPs should:

-

Consider the message they want to convey to stakeholders: Does your organization have ample resources to fund activities over the next 12 months? If yes – you want to make that clear in the disclosure. You may also want to discuss your policy for dealing with excess revenues (e.g., the board designates a certain percentage of excess budgeted funds to be added to the organization’s operating reserves). If your organization struggles to maintain sufficient resources to cover expenses, you may want to disclose your action plan for covering those expenses. Perhaps you have lines of credit that could be drawn upon if needed, or maybe you are expecting a large grant that will fund a significant portion of your expenses.

-

Review its current procedures around board designation of net assets: What are the board’s current procedures for identifying and designating net assets – are they formally documented, or are amounts designated by the board on an ad-hoc basis? Considering the board’s awareness of management’s designations is important, given the new standard’s emphasis on board designation of net assets. In addition to reviewing current procedures, this may be a good time for the board to revisit existing board designations to determine if they still make sense and determine if any new policies will be required.

-

Adopt an operating reserve policy if your organization doesn’t already have one. This policy would document (a) what the organization considers an appropriate level of reserves, (b) how the reserves will be built, and (c) the steps to follow if the reserves fall below the set level.

-

Decide on the best presentation approach for your organization. The format of the new liquidity disclosures will depend on the type of non-profit, the relative liquidity of the organization’s resources, donor-imposed restrictions on those resources, internal board designations on resources, and so on.

The non-profit may also consider adding or augmenting other disclosures. For example, suppose in your liquidity disclosures, you choose to break out the availability of promises to give into those that are donor-restricted and those that are not. In that case, consider whether providing the same breakout in your pledges receivable disclosure would be useful to the users of your financial statements.

We drew heavily from two articles prepared by the American Institute of CPAs (AICPA), including “The New Liquidity and Availability Disclosure and Going Concern Issues” and “Steps You Can Take Now to Create Exceptional Liquidity Disclosures.”

Profitability is an intuitive measure derived from changes in net assets (or change in net position). Recall that net assets increase when revenues exceed expenses – and vice versa.

The operating margin speaks to profitability in the organization’s core operations (i.e., change in net assets without donor restrictions). Gross margin (sometimes called margin) is the difference between net sales and cost of goods sold. Industries like retail clothing have extraordinarily tight margins, meaning the price often exceeds unit costs by a percent or two. Low-margin businesses must be “high volume,” meaning they must sell a lot of products to be profitable. Professional services like accounting, tax consulting, and equipment leasing are “high margin,” meaning the price charged far exceeds the unit cost, sometimes by orders of magnitude. High-margin industries tend to have barriers to entry. They require highly trained professionals, expensive equipment, or other significant up-front investments.

The total margin is a broader measure of profitability across the entire organization. For non-profits, the total margin accounts for all activities reported in the year, regardless of the restriction. For governments, the total margin incorporates the change in the net position of business-type activities. For for-profit or hybrid organizations, total margin accounts for all expenses before interest, taxes, depreciation, and amortization, frequently referred to as “EBITDA” (e-bit-dah).

There are caveats to the total margin ratio – particularly for governments and non-profit organizations. Organizations that receive funding with donor restrictions are more likely to report a total margin ratio greater than their operating margin. As noted in Chapter 2, change in net assets has two components – net assets without donor restrictions and net assets with donor restrictions. The total margin includes the latter, even though the organization will need to expend those resources at a future date or are restricted in perpetuity. Using the organization’s total margin ratio would incorrectly signal the non-profit’s profitability.

FINANCIAL STATEMENT RATIOS FOR PROFITABILITY |

||||

RATIO |

WHAT IT TELLS US |

NON-PROFIT |

GOVERNMENT |

FOR-PROFIT/HYBRID |

Operating Margin |

Do operating revenues cover operating expenses? Rule of Thumb: Positive | Change in Net Assets Without Donor Restrictions / Revenues Without Donor Restrictions | (Net Revenue or Expense for Governmental Activities / Total Revenues Governmental Activities Expenses)(x -1) | (Sales – Cost of Goods Sold) / Sales |

Total Margin |

Do total revenues exceed total expenses? Rule of Thumb: Positive | Change in Net Assets / Total Revenue | Change in Net Position for Primary Government / Total Revenue for Primary Government | Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) / Total Revenue |

Return on Assets |

How well does management leverage its assets to generate profits? Rule of Thumb: Positive | Change in Net Assets / Total Assets | Earnings Before Interest and Taxes / Total Assets | |

Return on Investments |

How well does management leverage its investments to generate income? Rule of Thumb: Positive | Investment Gain or Loss / Total Investments | ||

Return on Equity or Net Asset Growth |

What is the return on shareholders’ investments? Rule of Thumb: Positive | Change in Net Assets Without Donor Restrictions / Net Assets Without Donor Restrictionst-1 | Change in Governmental Activities Net Position / Net Position, Government Activities-1 | Net Income / Equity |

Own Source Revenue |

How much does this organization depend on support from other governments? Rule of Thumb: <10% | Primary Government Contributions / Primary Government Revenues | ||

Inventory Turnover |

How long does it take us to sell inventory? Rule of Thumb: <60 days | Inventory / (Cost of Goods Sold / 365 Days) | ||

For governments, the total margin ratio would include the change in the net position of their business-type activities. While business-type activities are self-sustaining, the profits cannot be used to subsidize the government’s core operations without legislative approval or a voter referendum. Consider the case of the City of Detroit when it filed for bankruptcy protection in 2013. City officials sought to transfer funds from its business-type activities (mainly funds in water and sewer) to the General Fund. Bondholders, secured with revenues from water and sewer services (i.e., business-type activities) sued and successfully prevented the transfer of funds to the General Fund, arguing resources are not fungible. Changes in law, contract, and administrative procedures would be required before resources are transferred from one fund to another.

Profitability measures are less salient for governments because governments need not be profitable to continue operating. Governments have the legal authority and monopolistic advantages that non-profits and for-profits do not. Governments can bolster their financial position by raising taxes or imposing fees. That’s why profitability measures for government are focused on not just the change in net position but the share of revenues derived from general revenues versus grants or contributions.

Solvency measures speak to where the organization gets its resources. Revenues – earned or contributed – pay for regular programming and operating expenses. Capital – loans and mortgages – are how an organization acquires its assets. If a non-profit depends too much on unpredictable or volatile donor revenues, that’s a potential solvency concern. The same is true of revenues from governments. Intergovernmental grants and contracts can disappear quickly if the government changes its fiscal policies and priorities.

Non-profits will report a wide variety of obligations, including accounts payable, accrued salaries and benefits, deferred revenue, long-term debt, and pension obligations. Since these are the result of doing business, they are expected and acceptable.

Although necessary, long-term debt is a drain on future resources. Research has shown that non-profits with long-term debt are less liquid and less profitable. An organization with long-term debt will make principal and interest payments every month (e.g., loans or mortgages) or semi-annually (e.g., bonds) – and, therefore, strain liquid resources and operating costs. Fixed assets frequently add to maintenance costs and depreciation expenses, resulting in lower profitability margins. These factors could inhibit an organization’s ability to continue to serve its mission.

The liability-to-asset ratio is an alternative measure of solvency. This ratio allows analysts to assess the scope of non-current liabilities that are not in the form of loans, mortgages, or bonded debt. For example, a significant proportion of liabilities reported by the Bill and Melinda Gates Foundation and the Susan G. Komen Breast Cancer Foundation were non-current grants payable. This reflects the organization’s use of multi-year grants to support the operating activities of other non-profits. The Boy Scouts of America, USA Gymnastics, and various Catholic dioceses have sizeable contingent liabilities following several recent sexual abuse lawsuits. These obligations are contingent on a court ruling or legal settlement. Accounting rules require organizations to report a contingent liability in the basic financial statements or notes to these financial statements. These disclosures depend upon the degree of certainty and materiality of the court ruling or legal settlement. These organizations will likely need to liquidate their existing assets to meet these obligations (as a side note, these organizations have filed for bankruptcy protection to allow for a negotiated settlement of outstanding obligations). The March of Dimes, Girls Scouts of America, American Civil Liberties Union, and the Metropolitan Opera Association all report an accrued pension liability. If the obligation is unfunded, it represents a drain on the organization’s resources.

We, therefore, encourage users to estimate a liability-to-asset ratio, keeping in mind that all debt is a liability, but not all liabilities are debt.

FINANCIAL STATEMENT RATIOS FOR SOLVENCY |

||||

RATIO |

WHAT IT TELLS US |

NON-PROFIT |

GOVERNMENT |

FOR-PROFIT/HYBRID |

Debt to Assets |

What percentage of this organization’s assets were financed with debt? Rule of Thumb: <0.5 | Total Debt / Total Assets | Total Debt / Total Assets | |

Liability to Assets |

What percentage of this organization’s assets are owed to third parties? (an alternative to debt-to-asset ratio) Rule of Thumb: <0.5 | Total Liabilities / Total Assets | Total Liabilities / Total Assets | |

Contributions Ratio |

How much does this organization depend on donors? Rule of Thumb: >10% but <75% | Total Contributions / Total Revenue | ||

Government Revenue Ratio |

How much does this organization depend on government funding? Rule of Thumb: <25% | Government Revenue / Total Revenue | ||

Near-Term Solvency |

How well can this government meet its near-term obligations with annual revenues? Rule of Thumb: <150% | (Total Liabilities – Deferred Inflows)Primary Government / Total RevenuesPrimary Government | ||

Debt Burden |

How much money has this government borrowed so far? Rule of Thumb: Depends | Total Long-Term DebtPrimary Government / Population | ||

Coverage 1 |

How easily can this government repay its debts as they come due? Rule of Thumb:<.15 | Debt ServiceGovernmental Funds / ExpendituresGeneral Fund | ||

Coverage 2 |

How easily can this government’s business-type activities repay their long-term debt obligations as they come due? Rule of Thumb: >5 | Operating RevenueProprietary Funds / Interest ExpenseProprietary Funds | ||

Capital Asset Condition |

Is this government investing in its capital assets? Rule of Thumb: Positive | (Net Investment in Capital Assetst – Net Investment in Capital Assetst-1) / Net Investment in Capital Assetst-1 | ||

The Internal Revenue Service (IRS) monitors the contributions ratio as part of its public support test for charitable organizations. According to this test, a non-profit must receive at least 10 percent of its support from contributions from the public or gross receipts from activities related to its tax-exempt purposes. Less than that suggests the public is not invested in that organization’s mission. By contrast, non-profit analysts also emphasize the tipping point where a non-profit depends too much on individual donors. Different analysts define the tipping point threshold differently, but most agree that 80 percent of total revenues from individual contributions is dangerously high. At that point, a non-profit’s ability to serve its mission is far too dependent on unpredictable individual donors and not dependent enough on either earned income (e.g., government contracts or fees-for-services) or gifts from corporations or foundations.

For governments, the solvency ratios are focused entirely on debt and other long-term obligations. Governments can borrow money that won’t be paid back for decades. If careless, a government can take on too much leverage. That is why solvency ratios for governments focus on how much money a government has borrowed or owes in its governmental and enterprise funds and its ability to meet those obligations as they come due. The latter is known as coverage. Bond investors, particularly for public utilities, often stipulate how much coverage a government must always maintain. Coverage ratios are usually expressed as operating revenues as a percentage of interest expenses.

In addition to financial health, financial statements can illuminate how efficiently a non-profit raises money and how much of its resources it devotes to its core mission. These effectiveness measures are related to but separate from the financial position. Fundraising efficiency shows the financial return a non-profit realizes for its investments in its fundraising capacity.

NON-PROFIT EFFECTIVENESS RATIOS |

||

RATIO |

WHAT IT TELLS US |

FORMULA |

Fundraising Efficiency |

What is the return on $1.00 in fundraising expenses? Rule of Thumb: >1 |

Total Contributions / Fundraising Expenses |

Program Expense Ratio |

What proportion of total expenses are invested in programs and services versus administration and fundraising? Rule of Thumb: > .8 | Program Expenses / Total Expenses |

The program expense ratio is one of the most closely watched and controversial ratios in non-profit financial management. It tells us how much of a non-profit’s total expenses are invested in its programs and services rather than administration, fundraising, and other overhead spending. Many analysts and non-profit monitors recommend a program service ratio of at least 80 percent – though we caution against the use of the program-expense ratio as allocation of expenses into program, administrative, and fundraising is far from clear cut.

RATIOS AND RULES OF THUMB

These rules of thumb are derived from the rich academic literature and industry analysis. To be clear, there is no legal or GAAP-based definition of “financially healthy” or “strong financial position.” Every financial institution, foundation, donor, or grantor defines these metrics differently. Measures of financial health will vary by sector and the size of the organization. The rules listed in the ratio tables above represent figures cited by analysts in the public and private sectors. Before going further, let’s consider a few key points about financial statement ratios:

- Ratios are only part of the story. Ratios are useful because they help us quickly and efficiently focus our attention on the most critical parts of an organization’s financial position. In that sense, they are a bit like watching ESPN’s 30-second highlight recap of a football game (or whatever sporting event, if any, you find interesting). If we want to know which team won and who made some big plays, we’ll watch the highlight reel. If we want to know the full story – the coaches’ overall game plan, which players played well throughout the game, when a key mistake changed the course of the game, etc. – we need to watch a lot more than just the highlights. Ratios are the same way. They are fast, interesting, and important. If we want a quick overview and not much more, they are useful. If we don’t have the time to dig deeper into an organization’s operations, or if it’s not appropriate for us to dig deeper, then they’re the best tool we have. But they are never the whole story. Always keep this limitation in mind.

- Always interpret ratios in context. Ratios are useful because they help identify trends in an organization’s financial behavior. Is its profitability improving? How has its overall liquidity changed over time? Are its revenues growing? And so on. But on their own, ratios don’t tell us anything about trends. To reveal a trend, we must put a ratio in context. We need to compare it to that same ratio for that same organization over time. For that reason, we often need multiple years of financial data. It is also essential to put ratios in an industry context. Sometimes, a broader financial trend will affect many organizations in similar ways. A decline in corporate giving will mean lower donor revenues for many non-profits. Increases in overall healthcare costs will impact all organizations’ income statements. Reductions in certain federal and state grants will affect particular types of non-profits in similar ways. To understand these trends, we need to compare an organization’s financial ratios to the ratios of organizations in similar industries. It is useful, for instance, to compare human services-focused non-profits with less than $2 million in assets to other small, human service-focused non-profits in the same region with less than $2 million in assets. We should compare fee-for-service, revenue-based non-profits to other fee-for-service, revenue-based non-profits. Large non-profits with national or international missions should be compared to each other.

- Financial statement analysis raises questions. A good financial statement analysis will almost always reveal some contradictory trends. Why does this organization’s profitability look strong, but the current ratio is well below the rule of thumb? Why is this organization less liquid than its peers? Why does this organization not have debt and is far more liquid than similar organizations? A good financial statement analysis raises questions about the organization’s financial assumptions, program operations, and overall effectiveness. Sometimes these follow-up questions can be answered from other publicly available information, such as the notes to the financial statements or the annual report. Sometimes they can’t. If your analysis concludes with many unanswered questions, that does not mean your analysis is bad. It simply means there are limits to what we can learn from financial statements alone.

- Ratios are retrospective. Most organizations release their financial statements three to six months after the close of their fiscal year. As a result, analysis based on those statements relies on information that is at least 12 to 18 months old. A lot can happen in 18 months! Always keep this in mind when doing financial statement analysis.

NON-PROFIT BUSINESS MODEL AND CAPITAL STRUCTURE

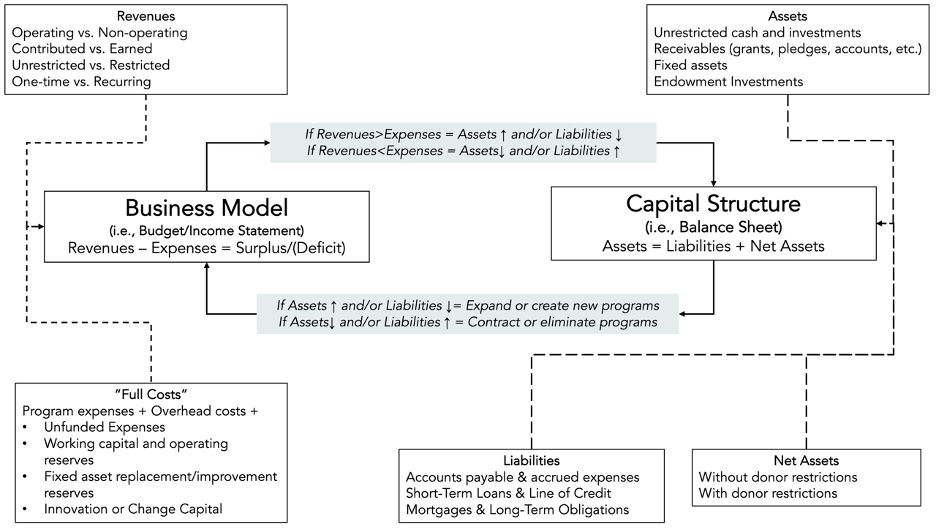

A non-profit’s financial self-assessment is based on a coherent analysis of the organization’s business model and capital structure. What do we mean by business model? It is the nature and distribution of an organization’s revenues and expenses. The business model reflects the non-profit’s strategic choices to fund operations (e.g., individual donors vs. corporate gifts, contributions vs. earned income, private support vs. government contracts) and resources allocated to programs and administrative services. A sustainable non-profit business model provides reliable revenues to cover the full cost of doing business. Sustainable non-profits understand how programs subsidize or are subsidized by others and maintain a specific, actionable plan to respond to unexpected events. Capital structure refers to the nature and distribution of an organization’s assets, liabilities, and net assets. A well-capitalized organization can access the cash necessary to cover its obligations, has the reserves to weather downturns in the external operating environment, and can take advantage of new opportunities to innovate.

We have modified the Non-profit Financial Assessment Toolkit developed by the Non-profit Finance Fund (NFF) to help non-profits assess their financial health. To contextualize questions included in the survey, let’s review the connection between an organization’s business model (i.e., Statement of Activities or Income Statement) and capital structure (i.e., Statement of Financial Position or Balance Sheet).

Thus far, we have focused on the idea that the non-profit’s revenues must meet or exceed program and overhead costs. However, a broader definition is necessary – one that accounts for the full costs of operations (a term we’ve also borrowed from NFF). Non-profits that generate enough resources to cover full costs of operations have sufficient reserves to meet unexpected costs or revenue shortfalls; can invest in technology, property, or equipment; and take advantage of new opportunities and are innovative in program or service delivery.

A non-profit’s ability to do so will be a function of the type of revenue it earns. Unrestricted contributions provide an organization with the greatest flexibility. Studies show that non-profits that rely on government contracts are more likely to report deficits and are more likely to be insolvent for two reasons. First, governments do not cover overhead costs. Failure to cover overhead costs means the organization has a structural deficit baked in the service agreement with the government agency. On the revenue side, the non-profit will need to raise additional donor support or rely on profitable ventures. On the expense side, the non-profit will likely scale back on administrative functions, including finance, technology, and other back-office staff. Eventually, it will need to draw down on reserves or cut back on critical program staff. Second, governments are more likely to delay payments. As a result, the non-profit will need to draw down on existing reserves, rely on lines of credit, or delay payments to vendors. It will forego investment income, incur an interest expense if it uses a line of credit, incur late payment penalties with vendors or suppliers, or forego pre-payment discounts.

A non-profit that consistently reports a surplus will see continued and sustained growth in assets. We’ll likely find that a significant proportion of its long-term obligations are used to acquire fixed assets (i.e., a mortgage or long-term debt). Those reporting a greater share of unrestricted public support are more likely to report a larger share of net assets without donor restrictions. That organization has a greater ability to expand programs. It can invest in new equipment, and excess funds can be transferred to a long-term investment portfolio that would generate investment income.

Non-profits reporting deficits are more likely to report fewer assets, and their liabilities are likely to grow over time. How does this happen? In the short term, it will draw on reserves, but persistent deficits will likely result in increased reliance on lines of credit and delayed payments to suppliers and vendors. Deficits will demand cuts to critical program and administrative staff. The deficits may incentivize the organization to pursue profitable but non-essential programs to subsidize essential programs, resulting in mission drift. Over the long term, the organization could become vulnerable to after-the-fact audits and claw-backs for disallowed expenses as a result of significant cuts in grant administration and finance staff. These create unexpected and sizeable contingent liabilities. The non-profit could also report a growing pension liability if it fails to fund employee benefit programs adequately. Growth in liabilities reflects the organization’s inability to generate revenues sufficient to cover full costs.

The figure below shows the connections between the non-profit’s business model (i.e., revenues, program expenses, and overhead costs) and capital structure (i.e., assets, liabilities, and net assets). As we noted in Chapter 2, non-profits need to budget for reserves. We, therefore, reflect not just program expenses and overhead costs in “Full Costs” but also reserve needs for the organization. Practically speaking, a non-profit would need to report a surplus equal to five percent of operating revenues for 10 consecutive years to accumulate reserves equal to six months of operating expenses. Given the evidence that most non-profits report deficits, a mix of budget surplus and capital campaigns would be necessary to create meaningful levels of reserves.

The more revenues (and, correspondingly, surpluses) a non-profit generates, the more assets it will report. Those will appear first in receivables and then in cash. Over time, these are invested in property and equipment or used to create informal or formal reserves.

Non-profits that are profitable can invest in or expand programs. Those that are not profitable will need to tap into reserves (i.e., cash and investments) in the short term or cut spending or sell assets over the long term to balance budgets and make payments on obligations as they come due. Selling assets and eliminating programs may be the only way the non-profit can maneuver out of a financial crisis.

Recommended readings include Morris, G., et al. (2018). The Financial Health of the United States Non-profit Sector: Facts and Observations, MacIntosh, J., et al. (2016). Understanding Overhead: A Governance Challenge for Non-profit Trustees and Nonprofit Finance Fund (2011) “Case for Change Capital in the Arts”

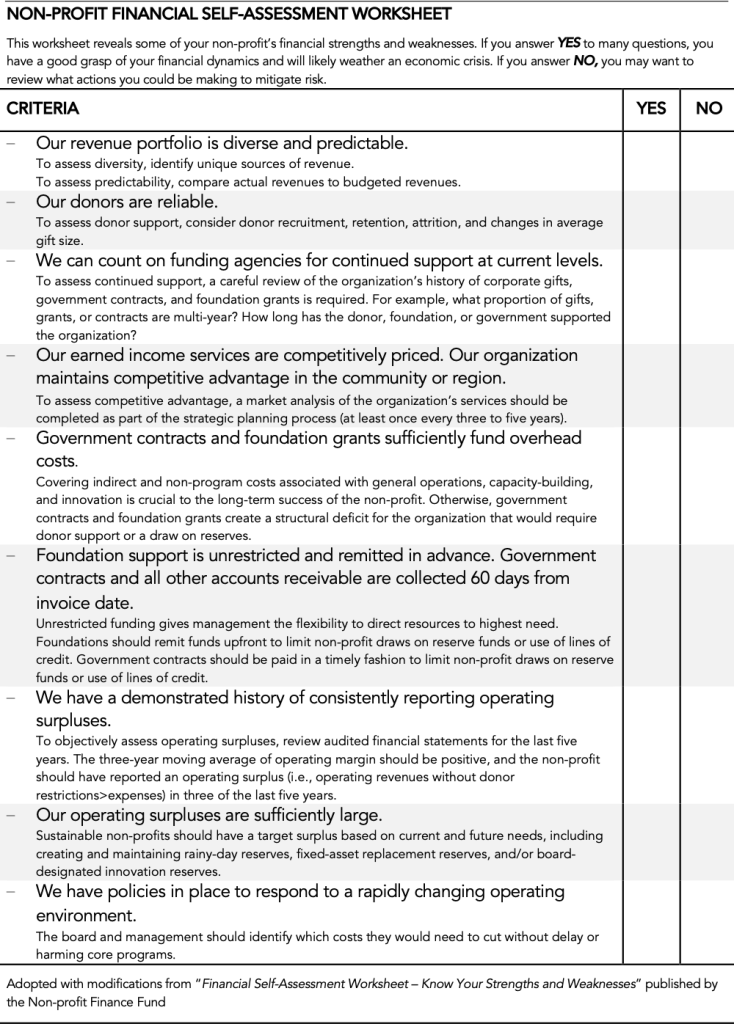

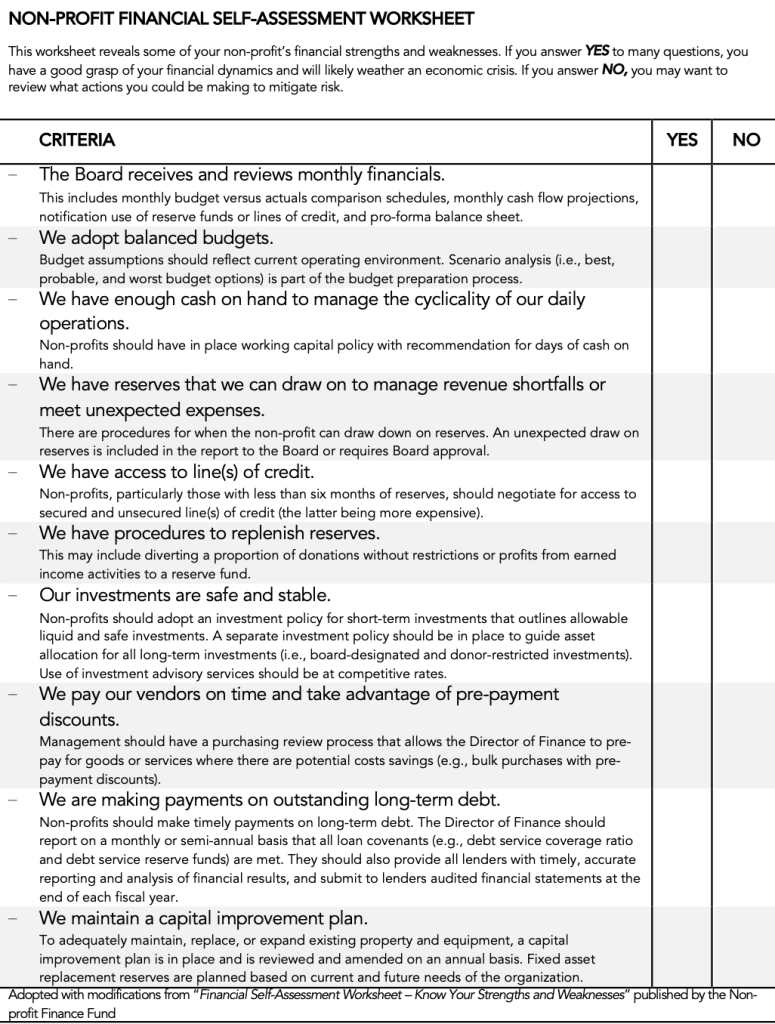

Download Non-Profit Financial Self-Assessment Worksheet: https://bit.ly/3rbVKUR

Download Non-Profit Financial Self-Assessment Worksheet: https://bit.ly/3rbVKUR

NON-PROFIT FINANCIAL RATIOS – AN ILLUSTRATION

To see these ratios in action, let us return to Treehouse. We use FY 2022 data to illustrate how each ratio is estimated and include FY 2021 ratios for comparative purposes. We highlight the key findings below. Note that our discussion below does not focus on how one should interpret each ratio. Instead, we tell a story about the organization’s financial position and operating performance. That story – not the ratios – helps formulate questions and additional lines of inquiry. Notwithstanding, we’ve included comments in the tables to help you understand how to interpret each ratio.

FINANCIAL RATIOS – TREEHOUSE

FINANCIAL RATIOS – TREEHOUSE |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2022 RATIOS |

20211 |

Current Ratio |

Will near-term assets cover near-term obligations? Rule of Thumb: >2 | Current Assets / Current Liabilities | 13,095,728 / 1,239,911 = 10.56

For every $1 in current liabilities, Treehouse reported $10.56 in current assets. |

12.16 |

Quick Ratio |

Will the most liquid assets cover near-term obligations? Rule of Thumb: >1 | (Cash + Investments + Receivables) / Current Liabilities | (4,430,208 + 3,162,683 + 970,433 + 195,182 + 3,528,538) / 1,239,911 = 9.91

For every $1 in current liabilities, Treehouse reported $9.91 in cash and receivables. |

11.42 |

Cash Ratio |

Will cash and investments cover near-term obligations? Rule of Thumb: >1 | (Cash + Investments) / Current Liabilities | (4,430,208 + 3,162,683) / 1,239,911 = 6.12

For every $1 in current liabilities, Treehouse reported $6.12 in cash and investments. |

9.67 |

Days of Cash on Hand |

How many days of cash do we have? Rule of Thumb: >90 days | (Cash + Investments) / ((Total Expenses – Depreciation – Bad Debt Expense) / 365 Days) | (4,430,208 + 3,162,683) / ((23,499,527 – 286,274 – 33,567) / 365 Days) = 119.56 Days

Treehouse reported $7,6 million in cash and unrestricted investments sufficient to meet 119 days of operating expenses. |

255.24 Days |

Days of Liquid Net Assets |

How many days of liquid net resources do we have? Rule of Thumb: >180 days | (Net Assets Without Restrictions – Fixed Assets Net of Depreciation) / ((Total Expenses – Depreciation – Bad Debt Expense) / 365 Days) | (19,743,171 – 7,097,000 – 1,228,420) / ((23,499,527 – 286,274 – 33,567) / 365 Days) = 179.79 Days

Treehouse reported unrestricted liquid assets of 179 days. This is a very strong unrestricted liquid net asset position even though it reported $8.3 million in fixed assets. |

298.41 Days |

Receivables Turnover |

How long does it take us to collect receivables? Rule of Thumb: <60 days | Receivables / (Revenues / 365 Days) | (970,433 + 195,182 + 3,528,538) / (23,385,623 / 365 Days) = 73.2 days

In FY 2022, Treehouse reported a significant increase in receivables. As a result, the receivables turnover period is higher than in previous years. |

35.65 Days |

What do the financial statements and estimated ratios tell us about Treehouse’s financial position and performance? Treehouse reported a strong financial position. At the end of FY 2022, the non-profit reported $27 million in assets, including $7.6 million in cash and investments, $5 million in receivables ($4.7 million are due in the next 12 months), $8.3 million in fixed assets (net of depreciation), and $5.2 million in endowment investments. That said, the non-profit reported a $2.1 million drop in cash and investments. While the drop in cash and investments has a negative impact on the non-profit’s liquidity position, the liquidity ratios remain at or above recommended benchmarks.

Return on EquityWhat is the return on shareholders’ investments? Rule of Thumb: PositiveChange in Net Assets Without Donor Restrictions / Net Assets Without Donor Restrictionst-17,108,483 / 12,634,688 = 56%There was an increase in equity because of the in-kind donation of an interest in the building resulting in a 56 percent increase in net assets without restrictions (or $7.1 million).34%

FINANCIAL RATIOS – TREEHOUSE |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2022 RATIOS |

20211 |

Operating Margin |

Do operating revenues cover operating expenses? Rule of Thumb: Positive | Change in Net Assets Without Donor Restrictions / Revenues Without Donor Restrictions | 516,298 / 24,015,825 = 24%

Including non-operating and restricted income, Treehouse reported a $5.6 million total surplus equal to 24 percent of total revenues. |

22% |

Total Margin |

Do total revenues exceed total expenses? Rule of Thumb: Positive | Change in Net Assets / Total Revenue | 5,622,029 / 23,385,623 = 24%

Including non-operating and restricted income, Treehouse reported a $5.6 million total surplus equal to 24 percent of total revenues. |

31% |

Return on Assets |

How well does management leverage its assets to generate profits? Rule of Thumb: Positive | Change in Net Assets / Total Assets | 5,622,029 / 26,966,259 = 21%

Including non-operating and restricted income, Treehouse reported a $5.6 million surplus equal to 21 percent of assets. |

20% |

Return on Investments |

How well does management leverage its investments to generate income? Rule of Thumb: Positive | Investment Gain or Loss / Total Investments | -1,361,592 / (3,162,683 + 5,189,663) = -16%

Treehouse reported $1.4 million in losses from investments equal to 16 percent of the value of the investments, including endowment investments. |

13% |

Return on Equity |

What is the return on shareholders’ investments? Rule of Thumb: Positive | Change in Net Assets Without Donor Restrictions / Net Assets Without Donor Restrictionst-1 | 7,108,483 / 12,634,688 = 56%

There was an increase in equity because of the in-kind donation of an interest in the building resulting in a 56 percent increase in net assets without restrictions (or $7.1 million). |

34% |

Treehouse reported $516,298 in income at the end of FY 2022 – approximately 2 percent of operating revenues. Operating revenues in FY 2022 ($24 million) were up 75 percent. Much of the growth in revenues was driven by contracts, most of which were with the State of Washington. Contributions, grants, and in-kind donations increased 14 percent. The nonprofit’s expenses ($23.5 million) were also higher, particularly in program services. Changes notwithstanding, the non-profit had a program-expense ratio of 83 percent. Total Change in Net Assets for FY 2022 was $5.7 million, including $1.4 million in losses from investments – which mirrors outcomes in the broader financial markets and in-kind donation of an interest in the building ($7.1 million).

Unlike most health and human services organizations, Treehouse has no long-term debt, and its liabilities are modest ($1.2 million).

FINANCIAL RATIOS – TREEHOUSE |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2022 RATIOS |

20211 |

Liability to Assets |

What percentage of this organization’s assets are owed to third parties? (an alternative to debt-to-asset ratio) Rule of Thumb: <0.5 | Total Liabilities / Total Assets | 1,239,911 / 26,966,259 = $0.05

Treehouse reported a negligible amount in payables and other obligations (five cents for every dollar in assets held). Keep in mind Treehouse does not report any long-term debt. We, therefore, estimate a liability-to-asset ratio instead of a debt-to-asset ratio. |

$0.05 |

Contributions Ratio |

How much does this organization depend on donors? Rule of Thumb: >10% but <75% | Total Contributions / Fundraising Expenses | (9,400,113 + 662,156) / 23,385,623 = 46%

Forty-six percent of revenues are from grants and contributions (including in-kind contributions). |

70% |

Government Revenue Ratio |

How much does this organization depend on government funding? Rule of Thumb: <25% | Government Revenues / Total Revenue | 12,659,996 / 23,385,623 = 54%

The remainder of the revenues are from government contracts (54 percent). |

29% |

Fundraising Efficiency |

What is the return on $1.00 in fundraising expenses? Rule of Thumb: > 1 | Total Contributions / Fundraising Expenses | (10,040,113 + 662,156) / 2,262,043 = $4.73

For every $1 in fundraising expenses, the non-profit raised $4.73 in grants and contributions. |

$5.96 |

Program Expense Ratio |

What proportion of total expenses are invested in programs and services versus administration and fundraising? Rule of Thumb: > .8 | Program Expenses / Total Expenses | 19,577,929 / 23,499,527 = 83%

For every $1 in expenses, 83 cents are invested in providing services to the non-profit’s clients. |

76% |

Download Treehouse Financial Statement Analysis: https://bit.ly/44SwTTL

Treehouse’s investments in fundraising are productive. For every $1 in fundraising expenses, the non-profit raised at least $5.00 in contributions and grants over the last five years. What’s more, our analysis shows it collected those receivables in 60 days or less. This ratio is critical to non-profits that rely on government contracts. If payments are late, the non-profit will need to draw down on its cash reserves and investments to meet operating expenses until the next payment is received. Non-profits that rely on monthly contributions, particularly from small donors, report a collection period that is less than 30 days. The financial statements show a significant increase in contracts in FY 2022 (up from $3.9 million in FY 2021 to $12.7 million in FY 2022) that led to a 204 percent increase in contract receivables ($3.5 million). This increase in receivables could negatively impact cash flows.

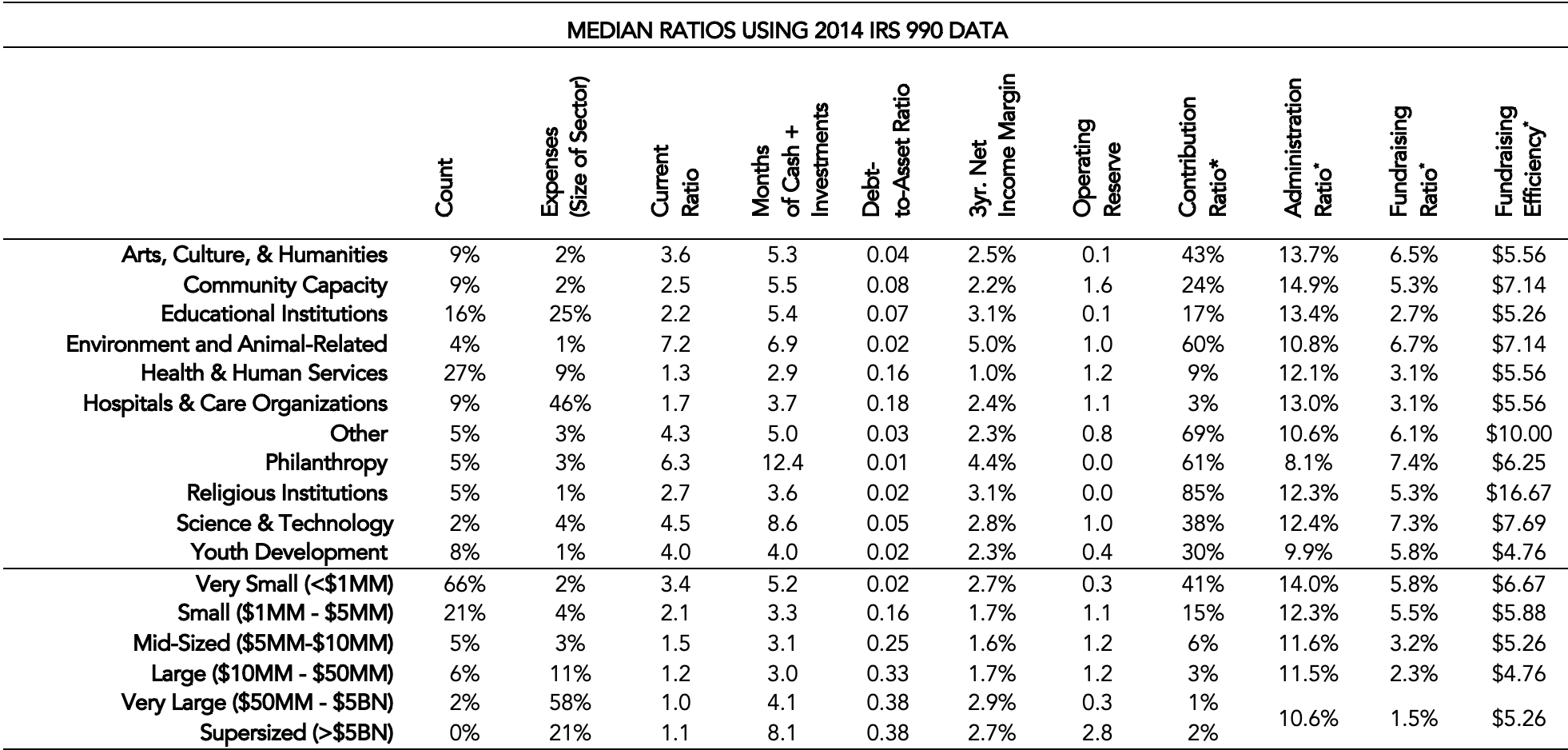

THE FINANCIAL HEALTH OF THE NON-PROFIT SECTOR

Unless specified, non-profit financial statements are prepared in accordance with GAAP. They are not, however, the only source of financial data. The IRS Form 990 provides the public with financial information comparable to that reported in the financial statements.

Form 990 is a unique blend of GAAP and tax-basis of accounting. For various reasons, the assets, liabilities, revenues, and expenses reported in the tax form 990 will differ from those reported in the financial statements. Limitations notwithstanding, the IRS maintains an electronic database that can be used to assess the financial health of the non-profit sector. Using 990 data reported by more than 200,000 non-profits reporting $2.45 trillion in expenses, Morris, Roberts, MacIntosh, and Bordone (2018) found the non-profit sector in the U.S. to be financially fragile, with non-profits in every sector frequently reporting deficits.

That research found:

-

Operating margins were largest for small non-profits (<$1 million), but there is significant variation in the data. For example, small non-profits were more likely to report large deficits or surpluses (the operating margin range was -21 percent to 32 percent). Large non-profits (>$10 million) were more likely to report a surplus. The distribution of operating margins was tighter (between -5.9 percent and 12.9 percent) and the largest non-profits (>$5 billion in expenses) did not report deficits.

-

Smaller organizations (<$5 million) are more likely to be liquid. While larger organizations (>$50 million) reported low current ratios, they maintain sizeable long-term investment portfolios, making them more resilient to an economic downturn. There was significant variation in liquidity by sector, with hospitals and human service organizations reporting low current ratios and reserve balances (and the lowest operating margins). Remember that these two sectors accounted for 55 percent of expenses and 36 percent of organizations. They represent organizations that underserved communities rely on.

-

Large non-profits (>$10 million in expenses) were more likely to report long-term debt. Not surprisingly, hospitals and health and human service organizations were more likely to report debt, as their business model mandates investment in property and equipment to meet the needs of the communities they serve. Philanthropic and environmental organizations reported the lowest debt burdens. These sectors were also the most profitable – 4.4 percent and 5.0 percent, respectively.

-

There are economies of scale with overhead costs, with larger non-profits reporting a lower share of overhead costs (i.e., administration and fundraising ratio). There were notable differences in fundraising ratios, with non-profits relying less on contributions reporting the lowest fundraising efficiency ratios and vice versa.

For detailed distributions of financial ratios, see Morris, G., et al. (2018). The Financial Health of the United States Non-profit Sector: Facts and Observations, Oliver Wyman, SeaChange Capital Partners, GuideStar and MacIntosh, J., et al. (2016). Understanding Overhead: A Governance Challenge for Non-profit Trustees, Oliver Wyman, SeaChange Capital Partners.

*Sample was limited to 10,754 non-profits in New York City. We believe the sample is sufficiently large and the results are representative of all non-profits. We transpose the author’s original estimate of fundraising efficiency ratio to estimate fundraising efficiency.

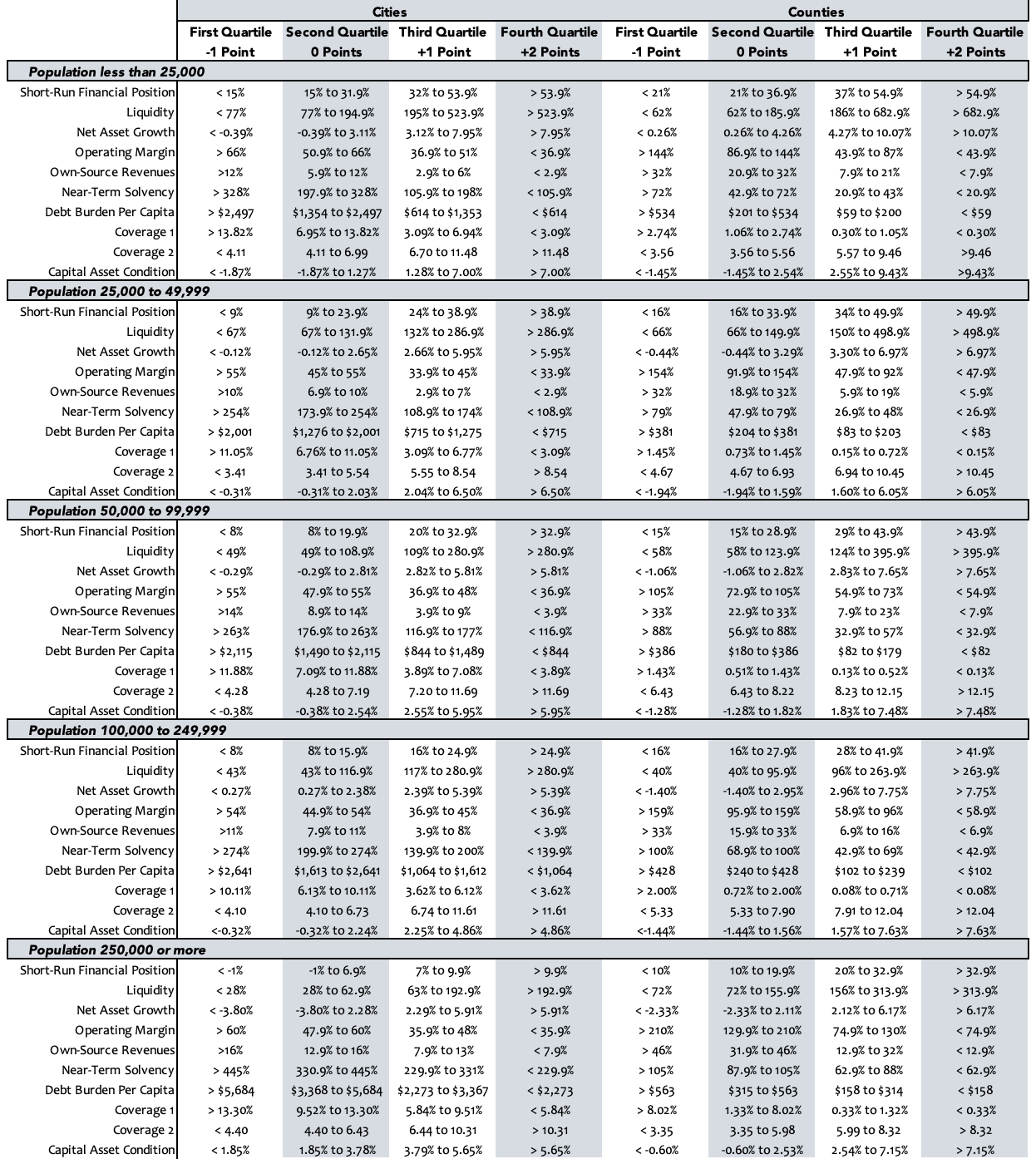

ASSESSING THE FINANCIAL HEALTH OF GOVERNMENTS USING THE TEN-POINT TEST

Throughout the past few decades, analysts have developed a popular framework to evaluate a local government’s financial condition. It is known as the “Ten Point Test.” It’s comprised of 10 key ratios that, when taken together, summarize a government’s liquidity, profitability, and solvency. In the Ten Point Test framework, a government earns “points” based on how its ratios compare to its peer governments. If its ratios are consistently better than its peers, it earns a higher score. If its ratios are consistently worse than its peers, its scores are lower and, in some instances, negative.

To see the Ten Point Test at work, let’s return to the City of Bothell. The table below shows the city’s ratios and their computations based on information in its 2021 Annual Comprehensive Financial Reports (ACFRs). Bothell’s 10-point ratios are a mixed bag. The government’s General Fund liquidity position is relatively strong. The city’s General Fund unassigned balance at the end of FY 2021 was $18 million (a historical high), approximately equal to 30 percent of the revenues reported in the General Fund. The government also reported $18.8 million in cash and investments (approximately 584 percent of its General Fund liabilities).

FINANCIAL RATIOS – CITY OF BOTHELL

FINANCIAL RATIOS – CITY OF BOTHELL |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2021 RATIOS |

2020 |

Short-Run Financial Position |

How much unrestricted resources do we have as a percent of our revenues? Rule of Thumb: >5% |

Unassigned General Fund Balance / General Fund Revenues | 18,021,012 / 61,009,245 = 30%

The City’s reported $18 million in unassigned General Fund balance at the end of FY 2021, approximately 30 percent of revenues reported in the General Fund – a historical high. |

20% |

Liquidity |

Will cash and investments cover near-term obligations? Rule of Thumb: >100% | (General Fund Cash + General Fund Investments) / General Fund Liabilities, excluding Deferred Inflows | (12,863,100 + 5,974,970) / 3,228,070 = 584%

The City reported $18.8 million in cash and investments, nearly six times the recommended liquidity position (584%) and the strongest liquidity position in more than five years. |

388% |

That said, the ACFRs show that the City’s net position declined $2.1 million or 0.4 percent of the net position. The $2.1 million deficit was a fraction of what the city reported prior to the COVID-19 pandemic. A quick review of the financial statements shows that depreciation expense has increased over the years – reflecting the city’s investment in infrastructure. This is also evident in the ratio measuring capital asset improvement, which continues to be negative (-7 percent).

The city relies on general revenues – specifically property and excise taxes – to cover operating expenses. The city reported $4.1 million in operating grants and contributions, approximately 3.12 percent of primary government revenues. Intergovernmental transfers were higher in FY 2020 and FY 2021, reflecting the infusion of federal stimulus funds in the city’s operations. The city’s operating margin for governmental activities was 61 percent. This ratio is larger because the city reported a deficit. The ratio would be lower if expenses were lower or if the government had reported more in either program revenues or general revenues. Notwithstanding, strong revenue growth and effective management of the city’s expenses have allowed the city to improve its net position.

FINANCIAL RATIOS – CITY OF BOTHELL |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2021 RATIOS |

2020 |

Net Asset Growth |

What is the return on shareholders’ investments?

Rule of Thumb: Positive |

Change in Governmental Activities Net Position / Net Position, Governmental Activitiest-1 | -2,095,559 / 598,097,828 = -0.4%

For every $1 in current liabilities, Treehouse reported $6.12 in cash and investments. |

-1.8% |

Operating Margin |

Do operating revenues cover operating expenses? Rule of Thumb: Positive | (Net Revenue or ExpensesGovernmental Activities / Total RevenuesGovernmental Activities)x-1 | (-65,848,816 / 107,267,488)x-1 = 61%

61 percent of the City’s operating expenses are supported by general revenues – primary property and excise taxes. As noted earlier, the city reported a deficit. That also means the city did not raise sufficient taxes to cover the full costs of operations. |

68% |

Own Source Revenues |

How much does this organization depend on the government? Rule of Thumb: < 10% | Primary Government Operating Contributions / Primary Government Revenues | 4,093,535 / 131,011,403 = 3%

Primary government operating grants and contributions were 3 percent of total revenues, significantly higher relative to prior to the COVID pandemic reflecting the infusion of federal support to the core functions of the city. |

5% |

The city of Bothell reports a high debt burden ($2,637 per capita). The rapid growth in population and the city’s planned expansion in capital improvements have resulted in the growth in the debt per capita. The government’s capital improvements make the city more attractive, which would lead to a growth in residents, resulting in a growth in revenues. Notwithstanding, its near-term solvency ratio (120 percent) is below the benchmark – reflecting growth in economic activity and, as a result, revenues. More importantly, the city’s pension and OPEB obligations are a modest share of the city’s non-current liabilities ($8.1 million, or 6 percent of non-current liabilities).

Moody’s upgraded the city from Aa2 to Aa1 on October 11, 2019. The rating agency noted that the city “benefited from its inclusion in the Puget Sound area.” Factors that could lead to a rating downgrade include “deterioration in the city’s financial position” because of “material contractions of the city’s taxable base.” The COVID-19 pandemic did not have a material negative effect on the government’s revenues. The city’s revenue portfolio is inelastic. Property values have not changed significantly since the start of the COVID-19 recession, and the housing market remains competitive.

FINANCIAL RATIOS – CITY OF BOTHELL |

||||

RATIO |

WHAT IT TELLS US |

FORMULA |

2021 RATIOS |

2020 |

Near-Term Solvency |

How well can this government meet its near-term obligations with annual revenues?

Rule of Thumb: < 150% |

Total Liabilities, excluding Deferred InflowsPrimary Government / Total RevenuesPrimary Government | 157,206,831 / 131,011,403 = 120%

Primary government long-term obligations are 120 percent of primary government revenues. The ratio declined as a result of an increase in tax revenues and federal support. Liabilities of the city ($157 million) were at a historical high. |

124% |

Debt Burden |

How much more money has this government borrowed so far?

Rule of Thumb: It depends! |

Total Long-Term DebtPrimary Government / Population | 129,018,696 / 48,920 = $2,637

Outstanding long-term debt obligations of the city (i.e., general obligation and revenue debt, excluding pension and OPEB obligations) were $2,637 per capita. Growth in long-term debt obligations reflects the City’s investments in infrastructure. |

$2,565 |

Coverage 1 |

How easily can this government repay its debts as they come due?

Rule of Thumb: <25% |

Debt ServiceGovernmental Funds / ExpendituresGeneral Funds | 8,221,959 / 55,379,086 = 15%

Debt service (i.e., principal and interest payments on long-term debt) were 15 percent of General Fund expenditures. Note, we estimate the ratio using debt service from governmental funds as the city reports debt service in a separate debt service fund. |

15% |

Coverage 2 |

How easily can this government’s business-type activities repay their long-term debt obligations as they come due?

Rule of Thumb: >1 |

Operating RevenueProprietary Funds / Interest ExpenseProprietary Funds | 21,101,687 / 469,803 = 47x

Revenues from business-type activities (water, sewer, and stormwater) can cover interest costs 47 times over. |

40x |

Capital Asset Condition |

Is this government investing in its capital assets?

Rule of Thumb: Positive |

(Net Investment in Capital Assetst – Net Investment in Capital Assetst-1) / Net Investment in Capital Assetst-1 | (558,338,328 – 602,305,433) / 602,305,433 = -7%

The City’s Net Investment in Capital declined 7 percent. Said differently, the City’s investment in capital improvements was less than the rate of depreciation of existing assets. |

-2% |

Download Bothell Ten-Point Test: https://bit.ly/4684Kcj

Fortunately, the Ten-Point Test framework allows us to go a step further. Instead of asking how Bothell compares to generic benchmarks (or rules of thumb), we have the tools to compare Bothell to peer local governments. This allows us to make much more precise statements about the City’s financial position and operating performance.

Analysts typically make these peer comparisons by computing the Ten Point Test ratios for various local governments and assigning point values based on relative rankings. For example, to calculate Bothell’s Ten Point test score for FY 2017 – 2021, refer to the Ten-Point Test Scores table. This table shows national trends for these same ratios. These trends are based on data from the financial statements of 3,721 city governments and 1,282 county governments from FY 2005 to FY 2015.

The ratios are presented in quartiles. Recall that a quartile is a group of percentiles, and a percentile identifies a point in the distribution of that ratio. The table is organized by population groups. So, for instance, for cities with populations between 25,000 and 50,000 (Bothell’s peer group), the 25th percentile for the short-run financial position was eight percent. That means one-quarter of Bothell’s peer cities had short-run financial positions of less than nine percent, and three-quarters had short-run financial positions equal to or greater than nine percent. For all the ratios shown here, the first quartile starts at the lowest ratio and ends at the 25th percentile, the second quartile covers the 25th percentile through the 50th percentile, and the third quartile covers the 50th percentile through the 75th percentile. The fourth quartile includes all observations above the 75th percentile.

INSOLVENCY AND MUNICIPAL BANKRUPTCY

Extreme instances of fiscal distress could lead a municipal government to file for Chapter 9 bankruptcy protection. Having satisfied state-specific eligibility requirements, a municipality’s petition in federal bankruptcy court must demonstrate the municipality (a) is insolvent, (b) desires to implement a plan to adjust, satisfy, or discharge debts, (c) has either negotiated in good faith, attempted but failed to negotiate with creditors, or negotiations are impracticable prior to bankruptcy protection application, and (d) has filed for bankruptcy protection in good faith.

The burden of demonstrating insolvency is extremely difficult. It requires the municipality to demonstrate that it is unable to pay its obligations as they come due or provide an adequate level of services. In recent years, the courts have sought an expansive definition of insolvency. Municipalities must demonstrate

-

an inability to generate and maintain cash balances to pay all its obligations as they come due (i.e., cash insolvency),

-

an inability to create a balanced budget that provides enough revenues to cover expenditures that occur in the budget period (i.e., budget insolvency),

-

an inability to pay for its long-term obligations given its current taxing or revenue authority (i.e., long-run insolvency), and

-

an inability to provide services at the level and quality that are required for the health, safety, and welfare of the community (i.e., service-level insolvency).

There are no financial ratios to assess service-level insolvency. Rather, service-level insolvency is a qualitative assessment of a government’s ability to deliver essential services. Service-level insolvency is characterized by longer fire and emergency services response rates, high rates of violent crimes and low rates of clearance, abandoned and blighted structures and lots, and poor service delivery (e.g., polluted water systems, broken streetlights, closed parks, etc.). In other words, governments that are service-level insolvent are struggling to deliver essential services.